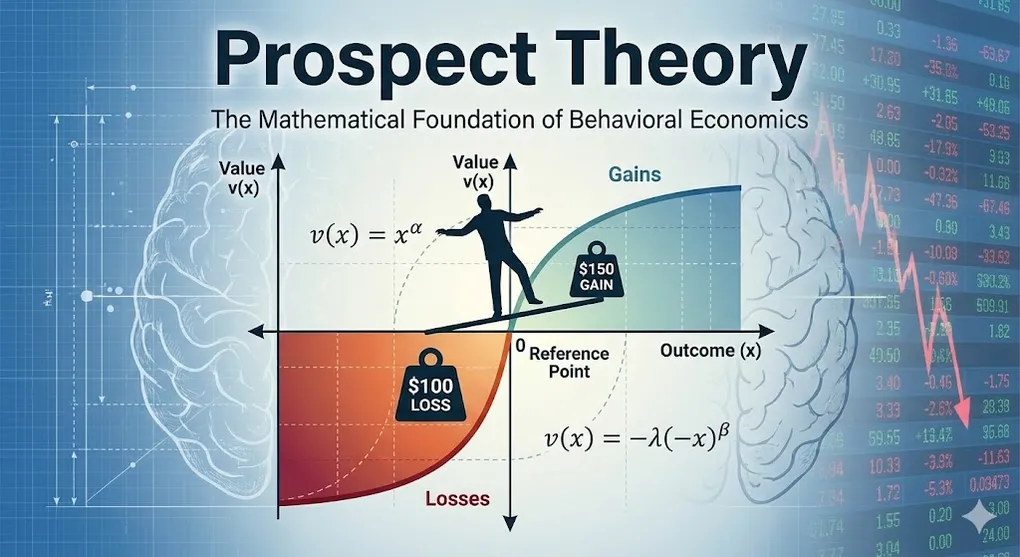

Prospect Theory: The Mathematical Foundation of Behavioral Economics

The Theory That Won a Nobel Prize

In 1979, psychologists Daniel Kahneman and Amos Tversky published a paper that would revolutionize economics: “Prospect Theory: An Analysis of Decision under Risk.”

Their insight? Humans don’t evaluate outcomes rationally. We don’t calculate expected utility like economists assumed. Instead, we use mental shortcuts that lead to predictable irrationality.

“Losses loom larger than gains.”

— Kahneman & Tversky, 1979

This single sentence captures decades of research and earned Kahneman the 2002 Nobel Prize in Economics.

The Problem with Expected Utility Theory

Traditional economics relies on Expected Utility Theory (EUT):

Expected Value = Σ (Probability × Outcome)Under EUT, a rational person evaluating a bet would:

- Calculate the probability-weighted value of each outcome

- Choose the option with the highest expected value

But humans don’t behave this way.

| EUT Prediction | What People Actually Do |

|---|---|

| Accept any positive expected value bet | Reject many favorable bets |

| Treat 100 lost | Feel losses ~2x more intensely |

| Evaluate outcomes independently | Compare to a reference point |

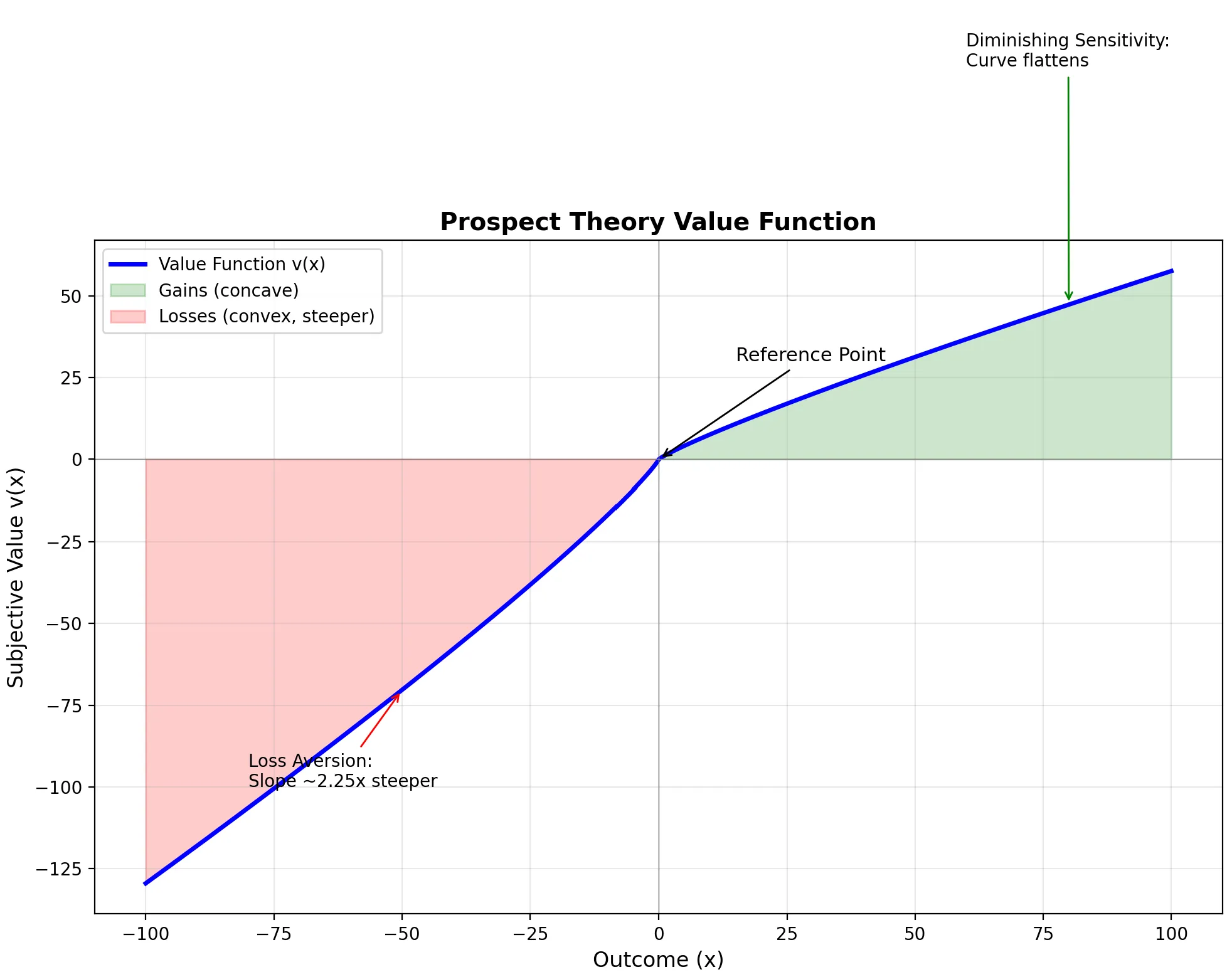

The Value Function: An S-Curve

The heart of Prospect Theory is the value function—a mathematical representation of how we perceive gains and losses.

Three Key Properties

| Property | Description | Implication |

|---|---|---|

| Reference Dependence | Value is measured relative to a reference point, not absolute wealth | Same outcome feels different depending on expectations |

| Diminishing Sensitivity | The curve flattens as magnitude increases | 200 feels bigger than 10,200 |

| Loss Aversion | The curve is steeper for losses than gains | Losing 100 feels good |

The Mathematical Formula

Kahneman and Tversky proposed this functional form:

Where:

- (diminishing sensitivity parameter)

- (loss aversion coefficient)

Visualizing the Value Function

Here’s Python code to plot the classic S-curve:

import numpy as np

import matplotlib.pyplot as plt

def prospect_value(x, alpha=0.88, beta=0.88, lambda_=2.25):

"""

Calculate subjective value according to Prospect Theory.

Parameters:

- x: outcome (gain if positive, loss if negative)

- alpha: diminishing sensitivity for gains (default: 0.88)

- beta: diminishing sensitivity for losses (default: 0.88)

- lambda_: loss aversion coefficient (default: 2.25)

"""

if x >= 0:

return x ** alpha

else:

return -lambda_ * ((-x) ** beta)

# Generate data points

x = np.linspace(-100, 100, 1000)

v = [prospect_value(xi) for xi in x]

# Create the plot

fig, ax = plt.subplots(figsize=(10, 8))

# Plot the value function

ax.plot(x, v, 'b-', linewidth=2.5, label='Value Function v(x)')

# Add reference lines

ax.axhline(y=0, color='gray', linestyle='-', linewidth=0.5)

ax.axvline(x=0, color='gray', linestyle='-', linewidth=0.5)

# Highlight key regions

ax.fill_between(x[x >= 0], 0, [prospect_value(xi) for xi in x[x >= 0]],

alpha=0.2, color='green', label='Gains (concave)')

ax.fill_between(x[x < 0], 0, [prospect_value(xi) for xi in x[x < 0]],

alpha=0.2, color='red', label='Losses (convex, steeper)')

# Annotations

ax.annotate('Reference Point', xy=(0, 0), xytext=(15, 30),

fontsize=11, arrowprops=dict(arrowstyle='->', color='black'))

ax.annotate('Loss Aversion:\nSlope ~2.25x steeper', xy=(-50, prospect_value(-50)),

xytext=(-80, -100), fontsize=10,

arrowprops=dict(arrowstyle='->', color='red'))

ax.annotate('Diminishing Sensitivity:\nCurve flattens', xy=(80, prospect_value(80)),

xytext=(60, 120), fontsize=10,

arrowprops=dict(arrowstyle='->', color='green'))

# Labels and styling

ax.set_xlabel('Outcome (x)', fontsize=12)

ax.set_ylabel('Subjective Value v(x)', fontsize=12)

ax.set_title('Prospect Theory Value Function', fontsize=14, fontweight='bold')

ax.legend(loc='upper left')

ax.grid(True, alpha=0.3)

plt.tight_layout()

plt.savefig('prospect_theory_value_function.png', dpi=150, bbox_inches='tight')

plt.show()

What the Graph Reveals

| Region | Shape | Behavior |

|---|---|---|

| Right of origin (Gains) | Concave (curves down) | Risk-averse for gains—prefer certain 100 |

| Left of origin (Losses) | Convex (curves up) | Risk-seeking for losses—prefer 50% chance of losing 50 loss |

| Steepness comparison | Losses ~2.25x steeper | Same magnitude loss hurts more than gain feels good |

Property 1: Reference Dependence

Our satisfaction depends not on absolute outcomes, but on comparisons to a reference point.

The Salary Paradox

| Scenario | Objective Outcome | Subjective Experience |

|---|---|---|

| You get 50K | +$100K | 😊 Thrilled |

| You get 200K | +$100K | 😤 Disappointed |

Same $100K. Completely different feelings. The reference point changed.

Practical Applications

| Domain | Reference Point Manipulation |

|---|---|

| Pricing | Show “was 99” to set higher anchor |

| Negotiations | First offer becomes the reference |

| Performance Reviews | Compare to department average, not absolute metrics |

Property 2: Diminishing Sensitivity

The value function is concave for gains and convex for losses. This means sensitivity decreases as you move away from the reference point.

The $100 Rule

| Change | Subjective Impact |

|---|---|

| 100 | HUGE |

| 1,100 | Noticeable |

| 10,100 | Barely register |

This has profound implications for decision-making.

Strategic Application: Segregate Gains, Integrate Losses

| Principle | Example |

|---|---|

| Segregate gains | Two 100 gift |

| Integrate losses | One 50 losses |

| Combine small loss with larger gain | ”500 purchase” feels better than “$400 total” |

UX Design Tip: Because of diminishing sensitivity, separating a painful process into smaller chunks doesn’t help—it might make it worse by resetting the reference point each time. But bundling “painful” payments into one single transaction (integration of losses) reduces total psychological pain.

This is why Amazon Prime works—one payment, zero shipping pain for the rest of the year.

Property 3: Loss Aversion (λ ≈ 2.25)

The most famous finding: losses hurt approximately 2.25 times more than equivalent gains feel good.

The Coin Flip Experiment

Would you accept this bet?

- Heads: You win $150

- Tails: You lose $100

Expected value: +$25. Most people reject this bet.

Why? The potential 150 gain.

For most people, you need to offer around 250 to win before they’ll risk losing $100.

Loss Aversion in Practice

| Domain | Manifestation |

|---|---|

| Investing | Disposition effect—selling winners too early, holding losers too long |

| Endowment Effect | Owning something increases its perceived value |

| Status Quo Bias | Preference for current state (change = potential loss) |

| Risk Premiums | Stocks must offer higher returns to compensate for volatility |

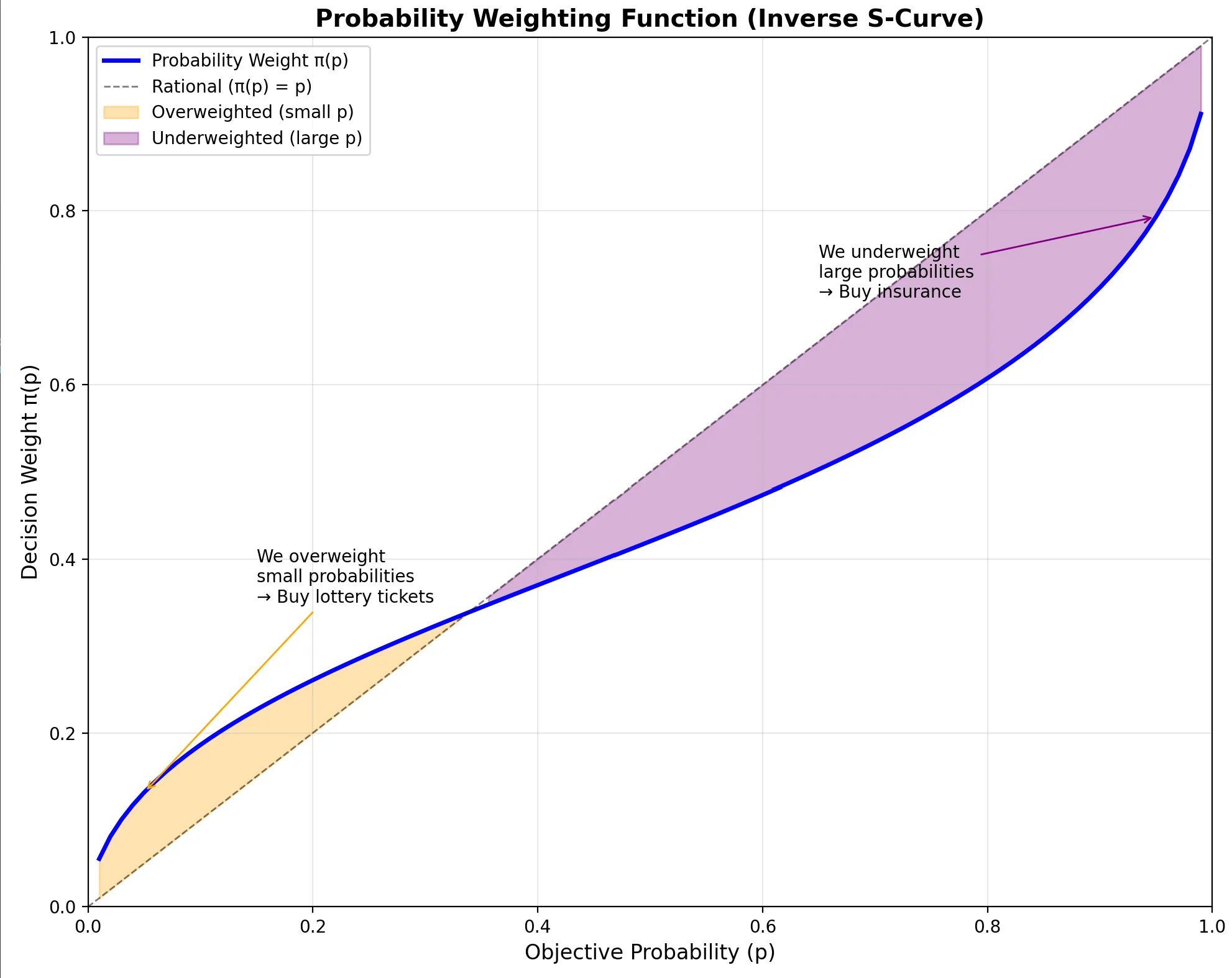

Advanced: Probability Weighting Function

Prospect Theory has a second component often overlooked: probability weighting.

We don’t perceive probabilities linearly either.

The Weighting Function

The probability weighting function transforms objective probabilities into subjective decision weights:

Where (curvature parameter from Tversky & Kahneman 1992).

Visualization Code:

import numpy as np

import matplotlib.pyplot as plt

def probability_weight(p, gamma=0.61):

"""

Probability weighting function from Prospect Theory.

Parameters:

- p: objective probability (0 to 1)

- gamma: curvature parameter (default: 0.61 from Tversky & Kahneman 1992)

"""

return (p ** gamma) / ((p ** gamma + (1 - p) ** gamma) ** (1 / gamma))

# Visualize the probability weighting function

p = np.linspace(0.01, 0.99, 100)

w = [probability_weight(pi) for pi in p]

fig, ax = plt.subplots(figsize=(10, 8))

# Plot the weighting function

ax.plot(p, w, 'b-', linewidth=2.5, label='Probability Weight π(p)')

# Reference line (rational = linear)

ax.plot([0, 1], [0, 1], 'k--', linewidth=1, alpha=0.5, label='Rational (π(p) = p)')

# Highlight overweighting and underweighting regions

ax.fill_between(p[p < 0.35], [probability_weight(pi) for pi in p[p < 0.35]], p[p < 0.35],

where=[probability_weight(pi) > pi for pi in p[p < 0.35]],

alpha=0.3, color='orange', label='Overweighted (small p)')

ax.fill_between(p[p > 0.35], [probability_weight(pi) for pi in p[p > 0.35]], p[p > 0.35],

where=[probability_weight(pi) < pi for pi in p[p > 0.35]],

alpha=0.3, color='purple', label='Underweighted (large p)')

# Annotations

ax.annotate('We overweight\nsmall probabilities\n→ Buy lottery tickets',

xy=(0.05, probability_weight(0.05)), xytext=(0.15, 0.35),

fontsize=10, arrowprops=dict(arrowstyle='->', color='orange'))

ax.annotate('We underweight\nlarge probabilities\n→ Buy insurance',

xy=(0.95, probability_weight(0.95)), xytext=(0.65, 0.7),

fontsize=10, arrowprops=dict(arrowstyle='->', color='purple'))

# Labels

ax.set_xlabel('Objective Probability (p)', fontsize=12)

ax.set_ylabel('Decision Weight π(p)', fontsize=12)

ax.set_title('Probability Weighting Function (Inverse S-Curve)', fontsize=14, fontweight='bold')

ax.legend(loc='upper left')

ax.grid(True, alpha=0.3)

ax.set_xlim(0, 1)

ax.set_ylim(0, 1)

plt.tight_layout()

plt.savefig('probability_weighting_function.png', dpi=150, bbox_inches='tight')

plt.show()

Key Distortions

| Objective Probability | Subjective Weight | Implication |

|---|---|---|

| Very small (0.1%) | Overweighted | We buy lottery tickets |

| Very large (99.9%) | Underweighted | We buy insurance |

| Moderate (40-60%) | Roughly accurate | Less distortion in middle |

Why We Buy Both Lottery Tickets AND Insurance

This seems contradictory:

- Lottery: Negative expected value, but we pay anyway

- Insurance: Often negative expected value, but we pay anyway

Prospect Theory explains both:

- Lottery: Overweight tiny probability of huge gain

- Insurance: Overweight tiny probability of catastrophic loss

The Fourfold Pattern of Risk Attitudes

Kahneman’s famous table explains how probability weighting + value function create four distinct behavioral modes:

| Probability | Gains | Losses |

|---|---|---|

| High (95%) | 🔒 Risk Averse | 🎲 Risk Seeking |

| Fear of disappointment | Hope to avoid loss | |

| Accept unfavorable settlement | Reject favorable settlement | |

| ”Take the sure 1000" | "Gamble to avoid $900 loss” | |

| Low (5%) | 🎲 Risk Seeking | 🔒 Risk Averse |

| Hope of large gain | Fear of large loss | |

| Buy lottery tickets | Buy insurance | |

| ”5% chance at $10,000? I’m in!" | "What if disaster strikes? I’ll pay.” |

Key Insight: The same person can be risk-seeking AND risk-averse—depending on whether they’re facing gains vs. losses and high vs. low probability. This is the Fourfold Pattern.

Detecting Prospect Theory in Data

As a data analyst, you can identify Prospect Theory effects in behavioral data:

1. Asymmetric Response to Gains vs. Losses

# Compare user reaction to equivalent gains and losses

def detect_loss_aversion(df):

"""

Detect loss aversion in user behavior data.

Expects columns: 'outcome_change', 'user_action_intensity'

"""

gains = df[df['outcome_change'] > 0]

losses = df[df['outcome_change'] < 0]

avg_gain_response = gains['user_action_intensity'].mean()

avg_loss_response = losses['user_action_intensity'].abs().mean()

loss_aversion_ratio = avg_loss_response / avg_gain_response

print(f"Loss Aversion Ratio: {loss_aversion_ratio:.2f}")

print(f"(Prospect Theory predicts ~2.25)")

return loss_aversion_ratio2. Reference Point Detection

Look for discontinuities at round numbers or historical benchmarks:

- Stock behavior around $100 price points

- Conversion rates around competitor pricing

- Performance changes around last year’s metrics

3. Diminishing Sensitivity Curves

Plot response intensity against outcome magnitude—look for the S-curve pattern.

Summary: The Complete Prospect Theory Framework

| Component | Formula | Key Insight |

|---|---|---|

| Value Function | (gains), (losses) | Asymmetric S-curve |

| Reference Dependence | evaluated relative to | Context matters more than absolute value |

| Diminishing Sensitivity | Concave gains, convex losses | Marginal impact decreases |

| Loss Aversion | Losses hurt 2x more than gains feel good | |

| Probability Weighting | overweights extremes | Small probabilities feel larger |

Further Reading

- 📄 Kahneman, D., & Tversky, A. (1979). Prospect Theory: An Analysis of Decision under Risk. Econometrica.

- 📄 Tversky, A., & Kahneman, D. (1992). Advances in Prospect Theory: Cumulative Representation of Uncertainty. Journal of Risk and Uncertainty.

- 📖 Thinking, Fast and Slow — Daniel Kahneman