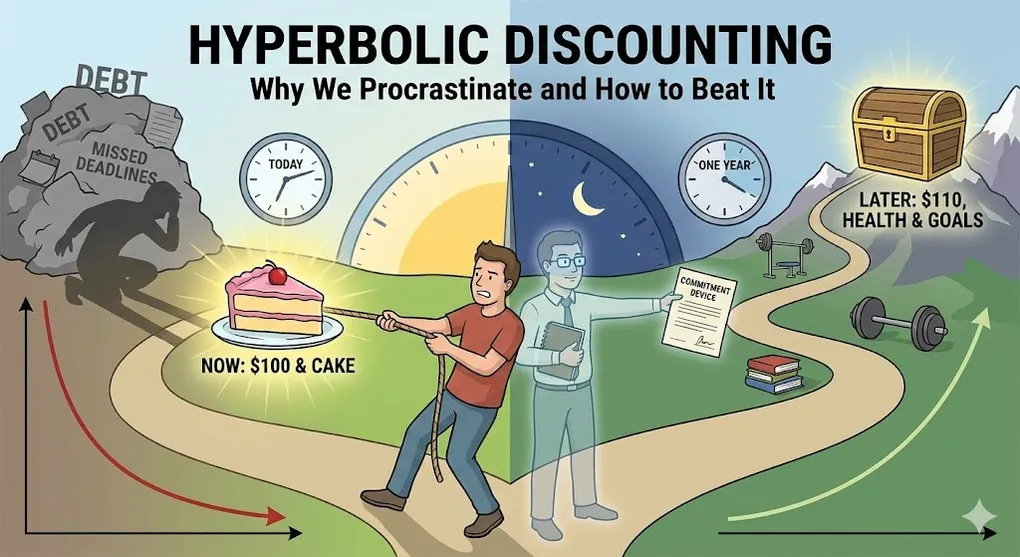

Hyperbolic Discounting: Why We Procrastinate and How to Beat It

The Procrastination Paradox

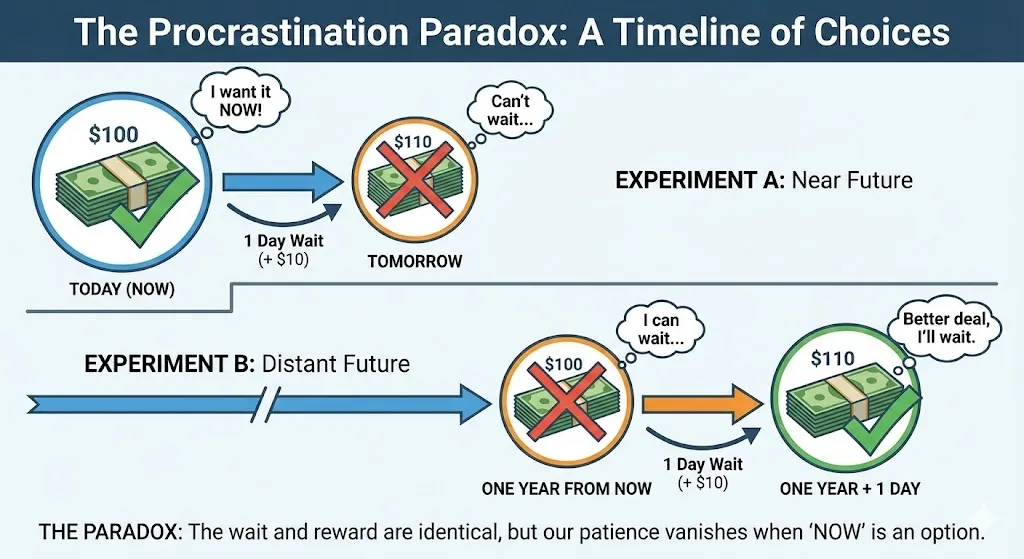

Consider these two choices:

Experiment A:

- Option 1: $100 today

- Option 2: $110 tomorrow

Most people choose today. We can’t wait.

Experiment B:

- Option 1: $100 in one year

- Option 2: $110 in one year and one day

Most people choose one year and one day. We’re happy to wait.

The paradox: Both scenarios involve waiting exactly one day for an extra $10. But our patience dramatically changes depending on whether “now” is involved.

This is hyperbolic discounting—and it explains everything from credit card debt to failed diets.

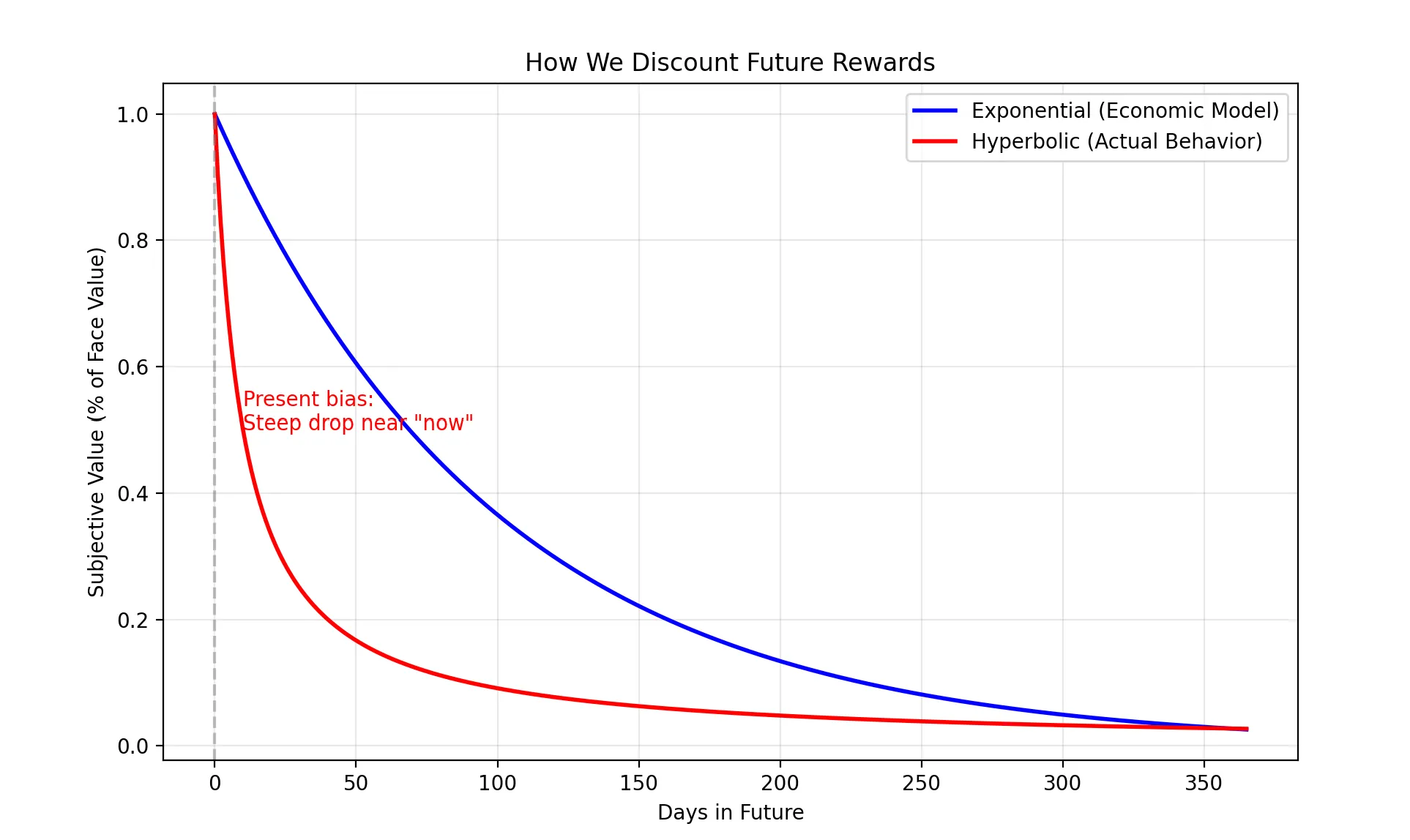

The Mathematics of Impatience

Traditional Economic Model: Exponential Discounting

Standard economics assumes we discount future rewards at a constant rate:

Where (delta) is a constant discount factor between 0 and 1.

Implication: If you’re willing to wait 1 day for $10 in one scenario, you should be willing in all scenarios.

Reality: Hyperbolic Discounting

Behavioral research shows our actual discounting follows a hyperbolic curve:

Where is an individual’s impulsivity parameter.

Visualizing the Difference

import numpy as np

import matplotlib.pyplot as plt

def exponential_discount(t, delta=0.99):

"""Standard economic discounting."""

return delta ** t

def hyperbolic_discount(t, k=0.1):

"""Behavioral discounting."""

return 1 / (1 + k * t)

# Time points (days)

t = np.linspace(0, 365, 366)

# Calculate present values

exp_values = [exponential_discount(day) for day in t]

hyp_values = [hyperbolic_discount(day) for day in t]

# Plot

plt.figure(figsize=(10, 6))

plt.plot(t, exp_values, 'b-', label='Exponential (Economic Model)', linewidth=2)

plt.plot(t, hyp_values, 'r-', label='Hyperbolic (Actual Behavior)', linewidth=2)

plt.xlabel('Days in Future')

plt.ylabel('Subjective Value (% of Face Value)')

plt.title('How We Discount Future Rewards')

plt.legend()

plt.grid(True, alpha=0.3)

plt.axvline(x=0, color='gray', linestyle='--', alpha=0.5)

plt.annotate('Present bias:\nSteep drop near "now"',

xy=(10, 0.5), fontsize=10, color='red')

plt.savefig('hyperbolic_discounting.png', dpi=150)

plt.show()

The Key Insight

| Time Frame | Hyperbolic | Exponential |

|---|---|---|

| Near future (today vs. tomorrow) | Steep discount | Gradual discount |

| Far future (year vs. year+1 day) | Flat (almost equal) | Same gradual discount |

The hyperbolic curve is steep near the present but flat in the distant future. This creates dynamic inconsistency—our preferences reverse over time.

Why Did Evolution Wire Us This Way?

This seems irrational—but it made sense for our ancestors:

| Environment | Optimal Strategy |

|---|---|

| Ancestral (savanna) | Tomorrow is uncertain. A lion might eat you. Take rewards now. |

| Modern (stable) | Tomorrow is predictable. Future planning wins. |

The Mismatch: Our brains evolved for environments where “a bird in hand” was survival. In modern society, this ancient wiring becomes a bug—not a feature—making long-term planning systematically difficult.

Present Bias: The War Between Two Selves

Behavioral economist Richard Thaler describes this as a conflict between two selves:

| Self | Time Horizon | Goal | Behavior |

|---|---|---|---|

| The Planner | Long-term | Save money, eat healthy, exercise | Sets goals, makes plans |

| The Doer | Present moment | Immediate gratification | Eats cake, skips gym, buys impulsively |

The problem: The Planner makes decisions for the future, but the Doer executes in the present—when temptation is strongest.

Example: The Gym Membership Trap

| Planner (January 1st) | Doer (January 15th) |

|---|---|

| “I’ll go 4x per week!" | "It’s cold. I’ll start Monday.” |

| Signs up for annual membership | Visits 3 times total |

| Feels motivated | Feels guilty |

Result: Gyms profit from the gap between our planned and actual selves.

Real-World Manifestations

1. Financial Decisions

| Behavior | Explanation |

|---|---|

| Credit card debt | Instant purchase (Doer) vs. future payment (Planner’s problem) |

| Under-saving for retirement | Retirement is too abstract; spending is immediate |

| Payday loans | Extreme present bias makes 400% APR seem acceptable |

| BNPL (Buy Now, Pay Later) | Pleasure of buying (now) decoupled from pain of paying (later) |

📱 Case Study: BNPL Services

Services like Afterpay, Affirm, and Klarna are perhaps the most sophisticated exploitation of hyperbolic discounting in modern commerce:

| Moment | Experience |

|---|---|

| Purchase (Now) | Full dopamine hit of acquisition |

| Payment 1 (2 weeks) | Distant, abstract, “I’ll deal with it later” |

| Payment 2-4 | By now, sunk cost fallacy kicks in |

“BNPL services weaponize hyperbolic discounting by decoupling the pleasure of buying (Now) from the pain of paying (Later).”

The Numbers:

- BNPL users spend 18-30% more per transaction

- Late fees generate significant revenue (the Planner fails)

- Average BNPL user has 3+ active installment plans simultaneously

2. Health Decisions

| Behavior | Explanation |

|---|---|

| Overeating | Cake now > Weight consequences later |

| Skipping exercise | Rest now > Health benefits in months |

| Smoking | Nicotine hit now > Cancer risk in decades |

3. Productivity

| Behavior | Explanation |

|---|---|

| Procrastination | Easy task now > Hard task with future deadline |

| Last-minute cramming | Leisure now > Distributed study effort |

| Missed deadlines | Future deadline feels far away… until it’s tomorrow |

Commitment Devices: Pre-Committing Your Future Self

Since we know our “future self” will be weak, the solution is to restrict their choices in advance.

Definition: A commitment device is an arrangement you make today that locks in future behavior, making it costly or impossible to deviate.

The Logic

Present Self (rational, planning)

↓ Creates constraints

Future Self (tempted, present-biased)

↓ Forced to comply

Desired Outcome achievedExamples of Commitment Devices

| Goal | Commitment Device | Mechanism |

|---|---|---|

| Save money | Auto-transfer to savings account | Money moves before you see it |

| Save more money | Fixed deposits with early withdrawal penalty | Pain of breaking commitment |

| Lose weight | Bet money on weight loss (e.g., StickK.com) | Financial penalty for failure |

| Exercise | Pay for personal trainer in advance | Sunk cost motivates attendance |

| Quit smoking | Tell everyone you’re quitting | Social accountability |

| Meet deadlines | Public commitment with consequences | Reputation at stake |

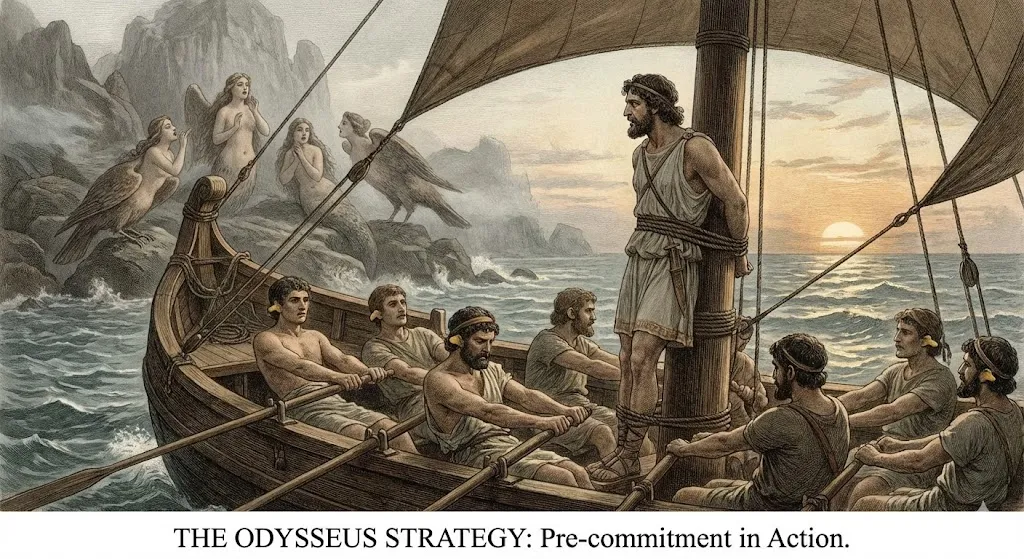

The Odysseus Strategy

The original commitment device: In Homer’s Odyssey, Ulysses ordered his crew to tie him to the mast so he could hear the Sirens’ song without jumping overboard.

The key insight: He recognized his future self would be weak and designed constraints in advance.

Designing for Hyperbolic Discounters

As a product designer or analyst, you can leverage (or combat) hyperbolic discounting:

Leveraging Present Bias (Ethically)

| Technique | Application |

|---|---|

| Immediate rewards | Gamification points, instant feedback |

| Make future benefits tangible | Show visualizations of compound interest |

| Reduce friction for good choices | Default to healthy option, savings plan |

Protecting Users from Present Bias

| Technique | Application |

|---|---|

| Cooling-off periods | Waiting period before large purchases |

| Pre-commitment features | ”Lock this savings account for 1 year” |

| Reminders at decision points | ”You said you wanted to save $500/month” |

Detecting Present Bias in Data

def detect_present_bias(user_behavior_df):

"""

Analyze user behavior for signs of hyperbolic discounting.

Look for:

1. High signup rates, low follow-through

2. Last-minute actions before deadlines

3. Preference reversal patterns

"""

# 1. Signup vs. Engagement ratio

signup_rate = user_behavior_df['signed_up'].mean()

engagement_rate = user_behavior_df['completed_action'].mean()

intention_action_gap = signup_rate - engagement_rate

# 2. Deadline clustering

deadline_actions = user_behavior_df[user_behavior_df['days_before_deadline'] <= 1]

last_minute_ratio = len(deadline_actions) / len(user_behavior_df)

print(f"Intention-Action Gap: {intention_action_gap:.1%}")

print(f"Last-Minute Action Ratio: {last_minute_ratio:.1%}")

if intention_action_gap > 0.3:

print("⚠️ High present bias detected: Users plan but don't follow through")

if last_minute_ratio > 0.5:

print("⚠️ Deadline clustering: Users procrastinate until last moment")

return {

'intention_action_gap': intention_action_gap,

'last_minute_ratio': last_minute_ratio

}The - Model: Formalizing Present Bias

Economists David Laibson and others developed a more precise model:

Where:

- (beta) = present bias parameter (typically 0.7)

- (delta) = standard discount factor

- = utility from consumption

Interpretation

| Parameter | Value | Meaning |

|---|---|---|

| No present bias | Standard economic agent | |

| Moderate present bias | Typical human | |

| Strong present bias | Impulsive individual |

When , we overweight immediate rewards relative to all future periods.

Summary

| Concept | Key Insight | Application |

|---|---|---|

| Hyperbolic Discounting | We discount near-future steeply, far-future flatly | Explains dynamic inconsistency |

| Present Bias | ”Now” has disproportionate weight | Planner vs. Doer conflict |

| Commitment Devices | Pre-commit to constrain future self | Auto-savings, penalties, accountability |

| - Model | captures present bias mathematically | Quantify individual impulsivity |

Further Reading

- 📄 Laibson, D. (1997). Golden Eggs and Hyperbolic Discounting. Quarterly Journal of Economics.

- 📖 Misbehaving — Richard Thaler

- 📖 The Willpower Instinct — Kelly McGonigal