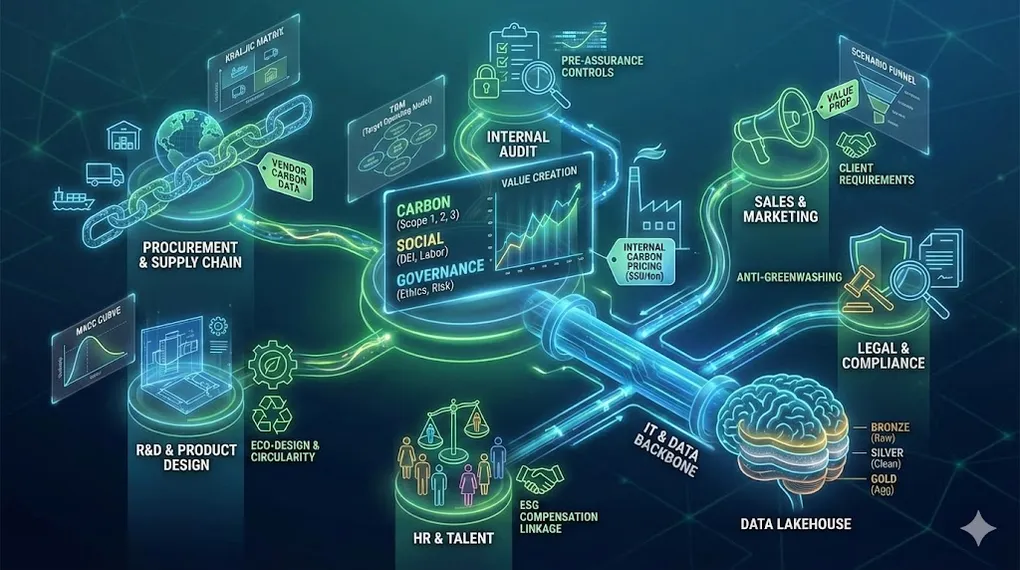

ESG Cross-Functional Impact: Departments, Strategy Models, and Data Engineering

With ISSB and stricter regulations (EU CBAM, CSDDD) coming into force, ESG has evolved from a “sustainability office” function to an “all-hands-on-deck” company-wide imperative.

If the financial statements are the scoreboard, then every department is a player on the field, either scoring or losing points. Finance can calculate all it wants, but if Procurement can’t source low-carbon materials and R&D can’t develop energy-efficient products, the final scorecard will still look bad.

Part 1: The Six Departments Most Impacted by ESG

1.1 Procurement & Supply Chain — The Scope 3 Gatekeepers

Impact Level: 🔴 Highest

This is the most pressured department during ISSB adoption and decarbonization efforts.

New Reality: Previously evaluated suppliers on “price, delivery, quality.” Now there’s a fourth criterion: carbon data.

| Change Area | What It Means |

|---|---|

| Supplier Screening | Must require carbon footprint data from suppliers. Non-compliant long-term partners may need to be replaced |

| Contract Negotiation | Supplier Code of Conduct clauses requiring emission reduction commitments and human rights compliance |

| Logistics Planning | Reducing transport emissions may require modal shifts (air → sea) or warehouse network redesign |

The Pain Point: Suppliers (especially SMEs) either can’t provide data or provide poor-quality data. Procurement becomes a “data collection agency” chasing reluctant vendors.

1.2 R&D & Product Design — Decarbonization at the Source

Core Driver: Eco-design

ISSB requires disclosure of “transition plans.” If your products are inherently high-emission, the company has no future.

| Change Area | What It Means |

|---|---|

| Material Substitution | Finding recycled or bio-based materials to replace virgin plastics—requires extensive testing |

| Design for Disassembly | Products must be easy to repair and recycle (circular economy compliance) |

| Energy Efficiency | Use-phase emissions (Scope 3 Category 11) are often the largest. “Power savings” becomes a core R&D KPI |

The Pain Point: Sustainable materials are usually more expensive or have inferior properties. R&D must painfully balance cost, performance, and sustainability.

Hardware Manufacturing Reality (Taiwan Context): Dell, HP, Apple now require not just green power at factories, but specific PCR (Post-Consumer Recycled) material percentages in products. R&D must ensure recycled materials can pass safety certifications and reliability testing—a significant engineering challenge.

1.3 Human Resources — Governance and the Talent War

Key ISSB Trigger: IFRS S1 explicitly asks: “Is executive compensation linked to sustainability performance?”

| Change Area | What It Means |

|---|---|

| Performance Metrics | 10-20% of executive bonuses may depend on “emission reduction target achievement” or “employee turnover rate” |

| DEI Disclosure | Must track and disclose gender pay gap, female leadership ratio, employees with disabilities |

| Talent Attraction | Gen Z talent heavily weighs company ESG image. ESG becomes core to employer branding |

The Pain Point: How do you quantify “Social” (S) metrics and tie them to bonuses? What weight should “employee satisfaction” carry? These debates get heated.

1.4 IT & Digital — The Data Infrastructure Backbone

Reality Check: ESG data used to live in scattered Excel files. Now it needs to be in the ERP.

| Change Area | What It Means |

|---|---|

| System Integration | Connect electricity bills, water bills, travel records, waste manifests to carbon management platforms |

| Audit Trail | Data must be immutable and traceable for assurance purposes. Every emission data point needs a source document |

| Cybersecurity | Now considered a Governance (G) issue—cyber vulnerabilities are material ESG risks |

The Pain Point: Classic “dirty work.” Data sources come in messy formats (PDFs, handwritten notes). Standardization is a nightmare.

1.5 Legal & Compliance — The Greenwashing Defense Line

New Risk: With anti-greenwashing regulations (EU Green Claims Directive) taking effect, misleading statements carry real penalties.

| Change Area | What It Means |

|---|---|

| Advertising Review | Marketing wants to say “100% eco-friendly.” Legal must demand evidence (ISO certification) before approval |

| Contract Review | Clarify carbon credit ownership, breach liabilities in supplier/customer agreements |

| Board Responsibility | Ensure directors understand their fiduciary duty regarding climate risk |

The Pain Point: Legal often becomes the “brake pedal” blocking Marketing’s exaggerated claims, creating cross-departmental tension.

1.6 Sales & Marketing — Client Requirements as License to Operate

B2B Reality: Without an ESG report, you may not even qualify to bid.

| Change Area | What It Means |

|---|---|

| Bid Qualification | Apple, Microsoft, TSMC require suppliers to commit to renewable energy. Sales must understand these requirements to win contracts |

| Product Carbon Footprint | Customers demand PCF for individual products. Sales coordinates with R&D and Manufacturing to calculate |

| Brand Premium | Marketing must convert “low carbon” into “high value” that customers will pay more for |

The Pain Point: Customer requirements are wildly varied—some want CDP, others want EcoVadis. Sales exhausts itself filling questionnaires.

1.7 Internal Audit — The Pre-Assurance Gatekeeper

Why Often Overlooked: Many companies focus on Legal/Compliance but forget that ISSB reports require third-party assurance.

| Change Area | What It Means |

|---|---|

| Internal Controls | Must establish controls over ESG data before external auditors arrive |

| Process Documentation | Every data point needs traceable SOPs (who collected it, when, how) |

| Readiness Assessment | Internal audit must test whether the organization can produce assurance-ready data |

The Pain Point: Internal audit teams trained in financial controls suddenly need to understand carbon accounting, emission factors, and Scope 3 estimation methodologies.

Part 2: Cross-Functional Collaboration Matrix

| Department | ESG Keyword | Core Task | One-Sentence Change |

|---|---|---|---|

| Finance | Capital Allocation | Calculate climate risk impact on financials | ”Not just managing money—managing carbon accounts too” |

| Procurement | Supply Chain Engagement | Collect supplier carbon data, purchase green power | ”Not just comparing prices—comparing emissions” |

| R&D | Eco-design | Develop low-carbon, recyclable products | ”Think about disposal during design” |

| HR | Compensation Linkage | Tie ESG targets to executive bonuses | ”Miss carbon targets, bonus gets cut” |

| IT | Digital Transformation | Build automated carbon accounting systems | ”Throw away Excel, automate the data” |

| Legal | Anti-Greenwashing | Verify all sustainability claims | ”No evidence, no ‘we’re eco-friendly’ claims” |

| Sales | Customer Requirements | Respond to ESG RFPs and questionnaires | ”No ESG report, no contract” |

| Internal Audit | Pre-Assurance Controls | Build ESG internal controls before external verification | ”If we can’t audit it internally, PwC will tear us apart” |

The Hardest Part: The biggest challenge in ESG integration isn’t technology—it’s communication across silos.

The “Clay Layer” Problem: Middle Management Resistance

Top executives want ESG. Junior employees support ESG. But middle managers—carrying quarterly KPIs (cost reduction, efficiency)—often see ESG as “creating trouble.”

| The Symptom | The Root Cause |

|---|---|

| Procurement manager keeps buying cheaper (higher-carbon) suppliers | KPI is 100% “Cost Down”—no weight on emissions |

| Factory manager resists process changes | Bonus tied to output volume, not carbon intensity |

| R&D leader delays sustainable material adoption | Time-to-market KPI doesn’t reward eco-design |

The Fix: If procurement manager’s KPI is still 100% cost-focused, they will never buy low-carbon but more expensive materials. ESG transformation requires KPI weight rebalancing at every level.

The Secret Weapon: Internal Carbon Pricing (ICP)

How do you make a factory manager care about emissions? Charge them for it.

By implementing a “Shadow Price” on carbon (e.g., $50/ton) in internal management accounts, high-carbon projects suddenly look less profitable.

| Scenario | Old Machine (High-Carbon) | Green Machine (Low-Carbon) |

|---|---|---|

| Before ICP | OPEX: $100K/year | OPEX: $120K/year |

| ROI: 5 years. Rejected. | ||

| After ICP ($50/ton) | OPEX: 30K carbon charge = $130K | OPEX: 5K carbon charge = $125K |

| ROI: 3 years. Approved. |

Why This Works: ICP is Finance’s most direct tool for influencing other departments. When carbon has a price on the internal P&L, procurement and operations managers automatically start optimizing for emissions—no moral persuasion required.

Part 3: Strategic Models — The Consultant’s Toolkit

When management consultants help companies with ESG transformation, they deploy a consistent set of frameworks.

3.1 MACC (Marginal Abatement Cost Curve) — Net-Zero Pathway Planning

Problem It Solves: You have 100 decarbonization options (change lightbulbs, buy green power, carbon capture, retrofit processes). Budget is limited. Which do you do first?

What It Looks Like: A bar chart ordered from left to right

| Axis | Meaning |

|---|---|

| X-Axis (Width) | Abatement potential (tons CO2 reduced) |

| Y-Axis (Height) | Abatement cost ($ per ton) |

How Consultants Use It:

| Zone | Interpretation | Recommendation |

|---|---|---|

| Negative Cost (below zero) | “Low-hanging fruit”—projects that save money (e.g., LED lighting) | Do immediately |

| Low Cost | Cheaper than carbon tax price | Include in medium-term plan |

| High Cost | Immature technology (green hydrogen, carbon capture) | Long-term R&D or wait |

Output: Helps CFO calculate ROI per dollar of decarbonization investment.

3.2 ESG Value Driver Tree — Financial Linkage Model

Based On: DuPont Analysis / ROIC Tree adaptation

Problem It Solves: Boss asks: “How exactly does ESG make us money?”

What It Looks Like: A tree diagram decomposing ROIC from left to right

| Value Driver | ESG Connection |

|---|---|

| Revenue Growth | → Green product premium, new market access (EU regulation compliance) |

| Operating Margin | → Energy efficiency savings, reduced waste disposal costs |

| Asset Turnover | → Early disposal of high-emission equipment |

| WACC | → Green financing rate discounts, lower risk premium |

Output: Translates abstract “sustainability” into concrete financial KPIs each department can own.

3.3 Climate Scenario Funnel — Risk Assessment

Based On: TCFD / ISSB Scenario Analysis requirements

Problem It Solves: Too many climate variables over 20 years. How do you forecast financial impact?

What It Looks Like: A funnel opening to the right with three pathways

| Pathway | Scenario | What Gets Assessed |

|---|---|---|

| Path A | 1.5°C (High Transition Risk) | Strict regulations, carbon price surge → Transition costs (carbon tax, technology investment) |

| Path B | >3°C (High Physical Risk) | Business as usual, planet heats → Disaster losses (factory flooding, supply chain disruption) |

| Path C | Chaotic Transition | Policy flip-flopping → Market volatility risk |

Output: Tells the board: “In the worst case, here’s how much we lose.”

3.4 TOM (Target Operating Model) — Organizational Design

Problem It Solves: Everyone says ESG is important, but no one is responsible, or departments point fingers at each other.

What It Looks Like: Roof diagram or onion chart with four layers

| Layer | Key Questions |

|---|---|

| Process | Who collects carbon data? Who reviews? (SOP design) |

| People | Who does CSO report to? Do departments need “Sustainability Ambassadors”? |

| Technology | What carbon accounting system to buy? How does it integrate with ERP? |

| Data | How are metrics defined? (Ties back to GHG Protocol) |

Output: Solves “who does what” and “with what tools.”

3.5 Sustainable Kraljic Matrix — Supply Chain Prioritization

Based On: Classic Kraljic Matrix, green upgrade

Problem It Solves: Thousands of suppliers. Which ones do I target for decarbonization first?

What It Looks Like: 2x2 quadrant

| Axis | Dimension |

|---|---|

| X-Axis | Supply Risk (replaceability) |

| Y-Axis | Spend Volume / Carbon Intensity |

| Quadrant | Description | Strategy |

|---|---|---|

| Strategic High-Carbon | High emissions, irreplaceable (wafer foundry, steel) | Deep engagement—collaborate on R&D |

| Non-Critical High-Carbon | High emissions, replaceable (logistics, packaging) | Mandate standards—switch if non-compliant |

| Low-Carbon Groups | Monitor only | Minimal attention |

Output: Focuses limited procurement resources on suppliers with highest decarbonization ROI.

Part 4: How These Models Connect

┌─────────────────────────────────────────────────────────────────────────┐

│ THE ESG TRANSFORMATION FLOW │

│ │

│ ┌──────────────────┐ │

│ │ SCENARIO FUNNEL │ "Scare the boss" │

│ │ (Risk Assessment)│ → What's the cost of doing nothing? │

│ └────────┬─────────┘ │

│ │ │

│ ▼ │

│ ┌──────────────────┐ │

│ │ VALUE DRIVER │ "Entice the boss" │

│ │ TREE (ROI) │ → How much can we make by doing this? │

│ └────────┬─────────┘ │

│ │ │

│ ▼ │

│ ┌──────────────────┐ │

│ │ MACC CURVE │ "Plan the path" │

│ │ (Prioritization) │ → Which projects deliver best ROI first? │

│ └────────┬─────────┘ │

│ │ │

│ ▼ │

│ ┌──────────────────┐ │

│ │ TOM (Org │ "Execute" │

│ │ Design) │ → Who does what, with what systems? │

│ └────────┬─────────┘ │

│ │ │

│ ▼ │

│ ┌──────────────────┐ │

│ │ KRALJIC MATRIX │ "Supply Chain Focus" │

│ │ (Procurement) │ → Which suppliers to prioritize? │

│ └──────────────────┘ │

└─────────────────────────────────────────────────────────────────────────┘Part 5: The Data Analyst’s ESG Nightmare

For Data Analysts and Data Engineers, mandatory ESG reporting (ISSB) represents a data infrastructure disaster and rebuild. Past marketing or financial analytics dealt with clean, structured data from ERP or CRM. ESG data analysis is an entirely different world.

5.1 Data Sources: From Structured to Extremely Fragmented

The “Garbage In” Challenge

| Traditional Analysis | ESG Analysis |

|---|---|

| Sales data from ERP/POS, unified format | Electricity bills (PDF), water bills (paper), supplier questionnaires (Excel), IoT sensor data (JSON), employee travel records (travel agency systems) |

Analyst Pain Point: 80% of time spent on ETL and data cleaning. Only 20% on actual analysis.

New Skills Required:

- OCR (Optical Character Recognition) to automatically read invoices

- Tools: Azure Form Recognizer, AWS Textract, Google Document AI

- NLP (Natural Language Processing) to parse unstructured supplier responses

5.2 Granularity: From Annual Totals to Transaction-Level

The Traceability Requirement

| Past (GRI Era) | Present (ISSB/CBAM Era) |

|---|---|

| Read meter once a year, report total emissions | Need to know: “How much power did this machine use during the hour we produced this one screw?” |

Why Transaction-Level:

- Product Carbon Footprint calculations require per-unit traceability

- Every energy consumption record needs timestamp and geo-tag

- Emission factors vary by time (daytime solar = lower factor) and location

5.3 Calculation Logic: The “Dimension Disaster” of Emission Factors

This is what makes ESG data analysis unique. You’re not just aggregating data—you’re matching coefficients.

The Challenge:

You have 10,000 procurement items (paper, computers, cement...)

↓

You need 10,000 corresponding emission factors from external databases

(Ecoinvent, IPCC, GaBi...)

↓

Factors change (updated annually), vary by region (China-made ≠ Taiwan-made)New Skill: Build automated Mapping Tables with Fuzzy Matching algorithms to handle messy item descriptions.

Python Stack for Factor Matching:

# Common libraries for ESG data engineering

import pandas as pd # Data cleaning

from fuzzywuzzy import fuzz, process # String matching for factor lookup

from sklearn.impute import KNNImputer # Missing data imputation5.4 Data Imputation: From “Exact” to “Scientific Estimation”

Handling Uncertainty & Proxy Data

| Traditional Finance | ESG Analysis (Scope 3) |

|---|---|

| 1. No guessing. | Supplier won’t give data? ISSB allows—even requires—estimation |

Analyst Tasks:

- Build statistical models to fill data gaps

- Example:

Procurement Spend × Industry Average Factor = Estimated Emissions - Must document methodology and assumptions

- Calculate and tag Data Quality Score for every estimate

5.5 Multi-Dimensional Views: Data Modeling for Dual Reporting

Star Schema Implications

Every electricity consumption record (Fact Table) must link to two dimension tables:

| Dimension | Source |

|---|---|

| Location-Based Factor | National grid average |

| Market-Based Factor | Green energy certificates (RECs) |

BI Tool Challenge: Reports must be able to switch views with one click. This requires careful dimensional modeling in Power BI/Tableau backends.

5.6 The ESG Analyst Tech Stack

| Layer | Traditional Tool | ESG-Required Tool | Purpose |

|---|---|---|---|

| Data Collection | Excel, Email | RPA (Robotic Process Automation) | Auto-scrape utility websites, auto-email suppliers for questionnaire completion |

| Data Warehouse | ERP Database | Sustainability Data Lake | Store unstructured environmental data and emission factor libraries |

| Calculation Engine | SQL, Excel | Python/R (specialized libraries) | Carbon accounting packages for complex unit conversions |

| Visualization | Monthly PDF Report | Real-time Dashboard | Monitor live carbon intensity, trigger alerts when thresholds exceeded |

5.7 The Hardest Question: Climate Scenario Analysis

ISSB’s toughest requirement is climate scenario financial analysis. This is where analysts need to run Monte Carlo Simulations:

| Variable | Range |

|---|---|

| X: Future carbon price (20 years) | 200/ton |

| Y: Extreme weather factory downtime | 0 - 30 days/year |

| Z: Company revenue growth rate | -5% to +15% |

Target Function: Probability distribution of EPS impact

This isn’t

SUM()orAVERAGE()anymore. It requires building probability models.

5.8 The Mindset Shift

ESG transforms data analysis from a “rearview mirror” (analyzing historical financials) into a “windshield” (predicting future risks).

| Old Paradigm | New Paradigm |

|---|---|

| Descriptive: “What happened?” | Predictive: “What could happen?” |

| Clean data, clear answers | Messy data, uncertainty ranges |

| Internal systems only | External databases (emission factors, climate scenarios) |

| Report the past | Model the future |

Part 6: ETL/ELT & Cloud Architecture — The Infrastructure Revolution

ESG data characteristics (unstructured, external sources, audit-required) are fundamentally different from traditional enterprise data (structured, internal, analysis-only). This directly impacts ETL/ELT design logic and cloud architecture decisions.

6.1 ETL vs. ELT: From “Clean Then Store” to “Evidence First”

Traditional BI uses ETL (Extract-Transform-Load): clean data first, then store. But for ESG, because of third-party assurance requirements, ELT (Extract-Load-Transform) has become mandatory—evolving into ELT-L (Extract-Load-Transform-Lineage).

| Aspect | Traditional BI (ETL) | ESG Reporting (ELT + Lineage) | Why |

|---|---|---|---|

| Raw Data Handling | Filter noise, keep only cleaned data | Must preserve original files (Raw Data Preservation) | Auditors demand “original water bill PDF” or “supplier’s raw Excel”—not just cleaned numbers |

| Transform Logic (T) | Hard-coded in scripts or SQL | Versioned and traceable | Emission factors update annually. You must explain “why 2023 used this factor, 2024 used that” |

| Error Handling | Overwrite after correction | Immutable + correction log | Once data is published, corrections must leave an audit trail—no silent overwrites |

6.2 The Medallion Architecture (Bronze-Silver-Gold)

ESG data pipelines typically enforce the Databricks Medallion Architecture:

┌─────────────────────────────────────────────────────────────────────────┐

│ ESG DATA LAKEHOUSE ARCHITECTURE │

│ │

│ ┌─────────────────┐ ┌─────────────────┐ ┌─────────────────┐ │

│ │ BRONZE (Raw) │→ │ SILVER (Clean) │→ │ GOLD (Agg) │ │

│ │ │ │ │ │ │ │

│ │ • Original PDFs │ │ • Unit convert │ │ • CO2e totals │ │

│ │ • Raw Excel │ │ (L→gal) │ │ • Power BI │ │

│ │ • IoT JSON logs │ │ • Standardize │ │ dashboards │ │

│ │ • IMMUTABLE │ │ names │ │ • ISSB reports │ │

│ └─────────────────┘ └─────────────────┘ └─────────────────┘ │

│ ↑ │

│ AUDIT EVIDENCE │

│ (Never modify) │

└─────────────────────────────────────────────────────────────────────────┘| Layer | Content | Rule |

|---|---|---|

| Bronze | Supplier Excel, PDF invoices, IoT raw logs | Immutable—audit evidence |

| Silver | Unit conversions, standardized supplier names | Versioned transformations |

| Gold | Combined with emission factors → final CO2e | Ready for reporting |

6.3 Data Pipeline Fragmentation

Traditional ETL sources are simple: SQL databases (ERP/CRM). ESG sources are a disaster:

| Source Type | Example | Challenge |

|---|---|---|

| IoT Sensors | Smart meters sending JSON every 15 minutes | High volume, real-time ingestion |

| External APIs | Google Maps (logistics distances), climate databases (physical risk) | Rate limits, authentication |

| Web Scraping | Utility company websites for latest emission factors | Fragile, format changes |

| Messy Files | Supplier questionnaires (hand-filled Excel, inconsistent formats) | Requires extensive cleaning |

Impact: Data Engineers must write more custom Python connectors instead of relying on standard SQL connectors.

6.4 The Dimensional Modeling Nightmare

Scenario: You have a purchase record—“100 tons of cement.”

Challenge: You can’t just multiply by a single fixed factor. During ETL, you must dynamically query:

| Question | Why It Matters |

|---|---|

| Where was this cement produced? | Taiwan factor ≠ China factor |

| When was it purchased? | 2023 factor ≠ 2024 factor |

| Did supplier provide a specific factor? | Use supplier-specific if available, else use industry average |

Technical Debt: This creates ETL scripts full of complex IF-ELSE logic and Lookup Joins.

6.5 Data Lineage: From “Nice to Have” to “Must Have”

Previously, Data Lineage was optional. Under ISSB, it’s mandatory.

Requirement: When an auditor clicks on “Scope 3 emissions: 50,000 tons” in your report, the system must draw a path showing which invoices contributed and which emission factor version was used.

Tool Impact: Companies are forced to adopt tools with strong lineage capabilities:

- dbt (data build tool) — Open source, SQL-based transformations with auto-documentation

- Informatica — Enterprise data governance with full lineage tracking

- Apache Atlas — Open-source metadata management

6.6 Cloud Architecture: The Rise of Data Lakehouse

Since ESG requires handling both structured data (ERP) and unstructured evidence (PDF invoices, images):

- Traditional Data Warehouse (structured only) → Not enough

- Pure Data Lake (no governance) → Too chaotic

Result: ESG is a major driver pushing enterprises toward Data Lakehouse architectures.

| Platform | Strength |

|---|---|

| Snowflake | Separation of compute/storage, easy scaling |

| Databricks | Native Medallion architecture, strong ML integration |

| Google BigLake | Unified analytics across formats |

6.7 Cloud ESG Products: Build vs. Buy

All three major cloud providers now offer vertical ESG solutions:

| Provider | Product | Focus |

|---|---|---|

| Microsoft | Cloud for Sustainability | Built on Dataverse, pre-built emission calculation models |

| AWS | Customer Carbon Footprint Tool | Calculates cloud infrastructure’s own carbon emissions |

| Salesforce | Net Zero Cloud | CRM data directly converted to carbon calculations |

Architect’s Dilemma: “Build custom on AWS with Python/SQL” vs. “Buy Microsoft’s SaaS”? Large enterprises typically choose hybrid: self-built Lakehouse at the bottom, SaaS for presentation layer.

6.8 GreenOps: The Meta-Problem

Here’s an ironic loop: Running ETL to calculate carbon emissions also generates carbon emissions.

New Discipline: Similar to FinOps (cloud cost optimization), GreenOps is emerging.

| Practice | Description |

|---|---|

| Carbon-Aware Scheduling | Run heavy ETL batch jobs or AI training during “green power windows” (e.g., midday solar peaks) or in regions with high renewable mix (e.g., hydro-rich regions) |

| Data Lifecycle Management | Delete cold data to reduce storage energy consumption |

| Right-Sizing | Don’t over-provision compute for ETL jobs |

6.9 Recommendations for Data Teams

-

Embrace ELT: Stop thinking “clean first, store later.” Store raw evidence first (Bronze Layer)—it’s your insurance policy for audits.

-

Obsess Over Metadata: Every data point needs tags (source, timestamp, factor version). Otherwise, next year’s recalculation will be a nightmare.

-

Upgrade Your Stack: Excel cannot handle Scope 3’s volume and complexity. Migrate to a modern data stack with version control (Git-based transformations like dbt).

Bottom Line: ESG isn’t just about reports—it’s redefining how enterprises trust their data. For data engineers, this is both a massive workload and a career-defining opportunity to become strategically important.

Conclusion: ESG Is Everyone’s Job Now

The message for 2025 and beyond is clear:

- Finance can’t do it alone—every department contributes to the final ESG score

- Cross-functional alignment is the biggest challenge, not technology or data

- Strategic frameworks help translate ESG from abstract ideals into actionable business plans

The companies that succeed will be those that treat ESG not as a compliance burden, but as an operating system upgrade that touches every function.