Behavioral Economics 101: The Psychology Behind Irrational Decisions

Why We Make Irrational Choices

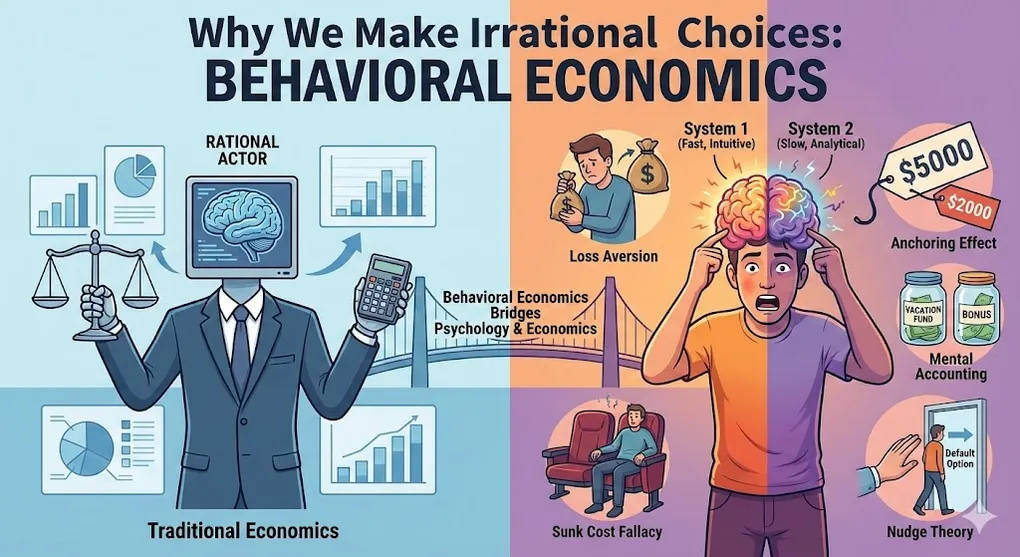

Traditional economics assumes humans are rational actors—that we carefully weigh costs and benefits before making decisions. Reality tells a different story.

Behavioral economics bridges psychology and economics to explain why smart people consistently make predictable mistakes. These aren’t random errors; they’re systematic biases hardwired into our brains.

“The agent of economic theory is rational, selfish, and his tastes do not change.”

— Richard Thaler, Nobel Laureate in Economics

Understanding these biases isn’t just academic—it’s essential for:

- Investors avoiding emotional trading mistakes

- Product managers designing better user experiences

- Analysts interpreting consumer behavior data

- Anyone wanting to make smarter decisions

The Two Systems: Fast and Slow Thinking

Before diving into specific biases, we need to understand how our brains process decisions.

Nobel laureate Daniel Kahneman introduced this framework in his seminal book Thinking, Fast and Slow:

| System | Mode | Characteristics | Example |

|---|---|---|---|

| System 1 | Fast Thinking | Automatic, intuitive, effortless, emotional | Recognizing a friend’s face; feeling fear at a loud noise |

| System 2 | Slow Thinking | Deliberate, analytical, effortful, logical | Calculating 17 × 24; filling out a tax return |

The Marketing Secret

Most purchasing decisions happen in System 1. Marketers know this.

Their goal? Keep your System 2 lazy or overloaded so System 1 makes the impulsive call.

| Tactic | Why It Works |

|---|---|

| Limited Time Offer! | Creates urgency, bypasses analytical thinking |

| Only 3 left in stock | Triggers scarcity bias, forces quick decision |

| Recommended for you | Reduces cognitive load, System 2 stays asleep |

Five Key Cognitive Biases

🔴 1. Loss Aversion

Definition: The pain of losing something is approximately twice as powerful as the pleasure of gaining the same thing.

We’re wired to fear loss more than we desire gain.

Classic Example:

Would you accept this bet?

- 50% chance to win $150

- 50% chance to lose $100

Mathematically, this is a good bet (expected value: +100 loss feels more significant than the $150 gain.

In the Real World:

| Domain | Manifestation |

|---|---|

| Investing | Holding losing stocks too long (“I can’t sell at a loss”) |

| Negotiations | Focusing on what you’ll give up, not what you’ll gain |

| Product Design | Free trials work because returning the product = loss |

Data Analysis Tip: Look for asymmetric responses to gains vs. losses in user behavior data.

⚓ 2. Anchoring Effect

Definition: Our judgments are heavily influenced by the first piece of information we encounter—even if it’s irrelevant.

The initial number “anchors” our perception of value.

Classic Example:

A jacket with two price tags:

- Tag A: ~~2,000** (You: “What a deal!”)

- Tag B: $2,000 (You: “That’s expensive…”)

The 2,000 price.

In the Real World:

| Domain | Application |

|---|---|

| Pricing | Show “original price” before discount |

| Salary Negotiation | First number mentioned sets the range |

| Financial Analysis | Prior year metrics anchor expectations |

Data Analysis Tip: When presenting findings, be aware that the first metric you show will anchor stakeholder perceptions.

🧠 3. Mental Accounting

Definition: We categorize money into separate mental “accounts,” leading to irrational spending decisions.

Money is fungible—100 won in a lottery. But we don’t treat them the same.

Classic Example:

- Overtime earnings: Carefully saved, spent reluctantly

- Lottery winnings: Splurged immediately on luxuries

Same purchasing power, completely different behavior.

In the Real World:

| Mental Account | Typical Behavior |

|---|---|

| ”Bonus money” | Spent more freely |

| ”Vacation fund” | Protected, even when in debt |

| ”Sunk costs” | Drives irrational continuation |

Data Analysis Tip: Customer segments may respond differently to the same offer depending on how they mentally categorize the purchase.

💸 4. Sunk Cost Fallacy

Definition: Continuing an endeavor because of previously invested resources (time, money, effort), even when it no longer makes sense.

The rational approach: past costs are sunk—they shouldn’t influence future decisions. But we can’t help ourselves.

Classic Example:

You’ve watched 20 minutes of a terrible movie. Do you:

- A) Leave and do something enjoyable (rational)

- B) Stay because “I already paid for the ticket” (fallacy)

The ticket money is gone either way. The only question is: how do you want to spend the next 90 minutes?

In the Real World:

| Domain | Manifestation |

|---|---|

| Project Management | ”We’ve invested too much to cancel now” |

| Investing | Averaging down on failing positions |

| Careers | Staying in wrong job because of years invested |

Data Analysis Tip: When evaluating project continuation, exclude historical costs from the decision framework.

👉 5. Nudge Theory

Definition: Guiding people toward better decisions by designing choices—without restricting freedom.

Coined by Richard Thaler and Cass Sunstein, nudges leverage our biases for good.

Classic Example:

To increase retirement savings participation:

- Old approach: Employees must opt-in to 401(k)

- Nudge approach: Employees are auto-enrolled, can opt-out

Result? Participation rates jumped from ~50% to over 90%.

In the Real World:

| Nudge | Outcome |

|---|---|

| Default options | Organ donation rates vary 10x between opt-in vs opt-out countries |

| Social proof | ”Most guests reuse their towels” increases compliance |

| Simplification | Reducing form fields increases completion rates |

Design Principle: Don’t ask “How do I convince people?” Ask “How do I make the right choice the easy choice?”

Implications for Data Analysts

Understanding behavioral economics transforms how you interpret data:

| Traditional View | Behavioral View |

|---|---|

| ”Users aren’t converting" | "What friction is triggering loss aversion?" |

| "Pricing seems optimal" | "What anchor are users comparing against?" |

| "Feature isn’t being used" | "Is the default setting working against adoption?” |

Practical Applications

- A/B Testing: Test different anchors, not just different prices

- Funnel Analysis: Identify where loss aversion might cause drop-offs

- Segmentation: Group users by their behavioral patterns, not just demographics

- Dashboards: Be conscious of which metrics you anchor stakeholders to

Summary

| Bias | Core Insight | Counter-Strategy |

|---|---|---|

| Loss Aversion | Losses hurt 2x more than gains feel good | Frame changes as gains, not losses |

| Anchoring | First number sets expectations | Be intentional about your opening position |

| Mental Accounting | Money isn’t treated equally | Recognize artificial boundaries |

| Sunk Cost | Past investments cloud judgment | Focus only on future costs and benefits |

| Nudge | Choice architecture shapes decisions | Design defaults thoughtfully |

Further Reading

- 📖 Thinking, Fast and Slow — Daniel Kahneman

- 📖 Nudge — Richard Thaler & Cass Sunstein

- 📖 Predictably Irrational — Dan Ariely